TL;DR

- Manual loan underwriting causes 3–7 day delays, applicant drop-offs, and inconsistent decisions that fail to scale.

- AI underwriting software automates credit scoring in milliseconds using ML models and alternative data sources.

- A production-ready system relies on 5 components: data ingestion, feature engineering, model selection, explainability (SHAP), and continuous retraining.

- Explainability layers keep automated decisions compliant with regulations like the EU AI Act.

- Tensorway builds custom AI underwriting systems and delivers full IP ownership, a scoring API, compliance documentation, and automated retraining pipelines.

A borrower submits a consumer loan application with all the required documents uploaded, but then, the process freezes. The applicant waits three days for an approval decision that an ML model can calculate in milliseconds. Such a situation is quite typical for many organizations today.

This friction occurs because traditional underwriting still relies on a human queue. Just imagine a regional lender with three underwriters receiving 400 consumer loan applications per week. Manual processing remains the default failure point. To avoid this, fintech teams are moving toward automated AI underwriting software. This helps them scale origination volume without increasing the headcount.

In this article, we are going to talk about the peculiarities of loan underwriting automation, explain how AI lending solutions work, and share practical tips on how to build such systems based on our experience.

What Is AI Underwriting Software?

AI underwriting software is an automated infrastructure layer that uses machine learning models to score consumer loan applicationы. It can output both the final credit decision and the legally mandated adverse action reason codes.

It fundamentally replaces the spreadsheet-based credit policies and the archaic process that was based on manual data processing. The software executes the same risk checks, but it can do this in milliseconds and handle any application volume without performance degradation.

Across consumer lending (from personal loans and BNPL to auto financing and credit cards), the algorithmic logic is highly consistent. The system's behavior is dictated by the specific training data and the regulatory context of the asset class.

The deployment of an AI lending platform doesn’t eliminate the need for human oversight on complex edge cases. Algorithmic fairness requires continuous bias testing, and lenders remain accountable for their models.

Nevertheless, AI credit risk assessment significantly enhances the efficiency of traditional underwriting. In the table below, you can see a brief comparison of these two approaches to lending.

Why Does Manual Loan Decisioning Fail at Scale?

Manual human workflows often become structural failure points of lending workflows. In our practice, we often work with lenders and have detected the main operational vectors that are negatively impacted by manual processes.

Abandonment Loops and Growing Costs

In consumer lending, applicant drop-off spikes every hour a decision remains pending. Borrowers frequently apply across multiple fintech platforms simultaneously. Given this, a manual speed mismatch means you lose prime loans to a competitor that approves them first. The failure mode here is lost origination revenue and increasing acquisition costs that never convert.

Meanwhile, automation has an opposite effect. According to Freddie Mac’s 2024 Cost to Originate Study, fully digitized mortgage processes can help lenders save up to 40% in operational costs.

Decision Asymmetry

Manual credit verification is fundamentally subjective. The same applicant profile will often be viewed differently by two underwriters due to possible interpretations of discretionary criteria.

A lender can’t mathematically audit the precise weight of every variable across 50,000 historic decisions. At scale, these inconsistencies can lead to fair lending compliance issues.

Volume Ceilings

A sudden marketing cycle or macroeconomic shift can be a reason for a spike in your application volume. And a human underwriting team won’t be able to cope with it.

In such cases, you face devastating processing delays. To hire operators, you will need a couple of weeks for onboarding. As one of the Reddit users noted, “The real win is handling volume spikes and automating the straightforward cases so underwriters focus on complex applications.”

Disconnected Feedback Infrastructure

Manual lending setups can’t learn from past mistakes. If a borrower defaults 18 months after origination, there is no automated way to trace that loss back to the underwriter's original checklist and fix the criteria.

AI underwriting fixes this by creating a direct loop. It constantly tracks which loans get paid back and automatically updates its rules to make smarter decisions next time.

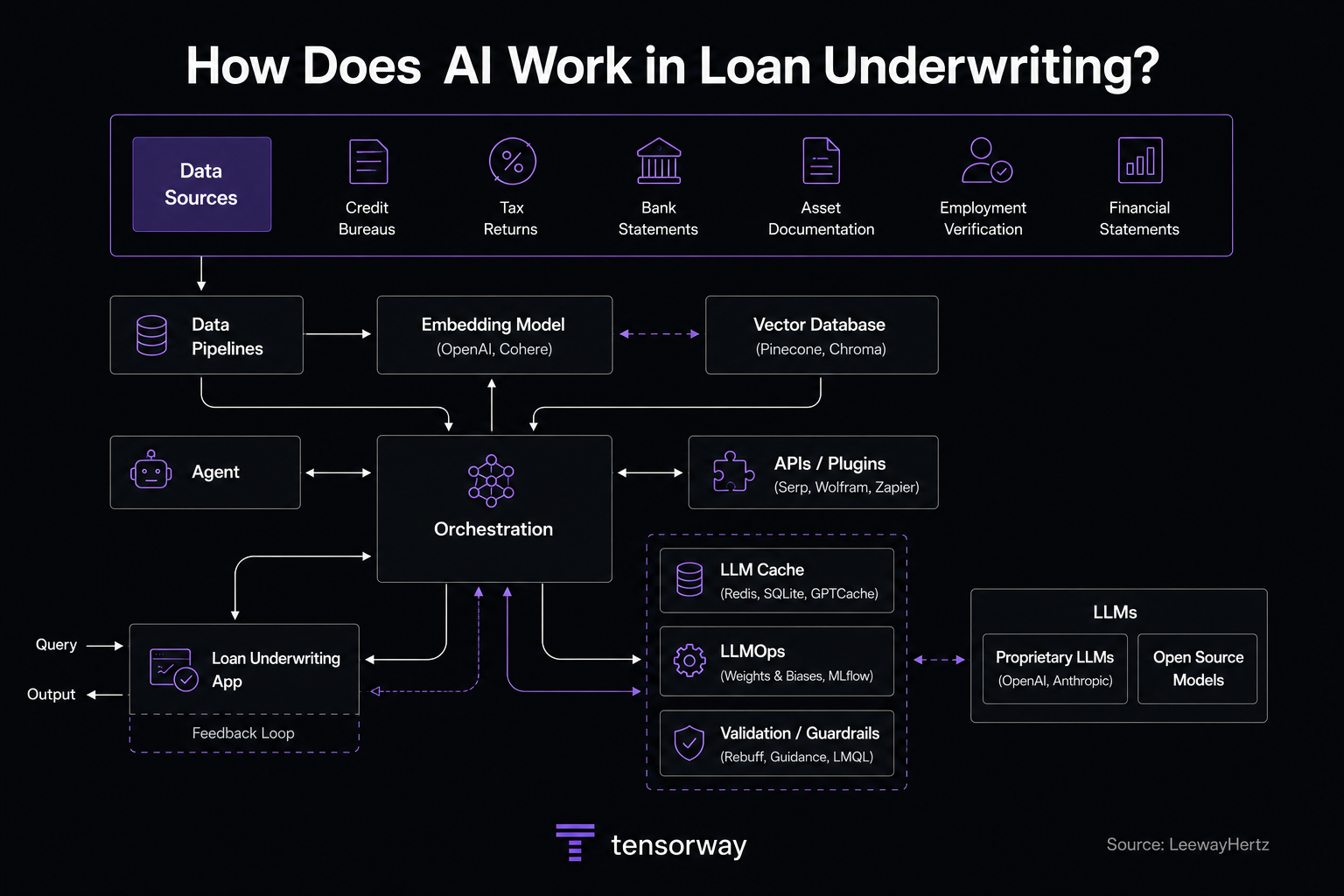

How Does AI Loan Underwriting Software Work?

Production-grade AI underwriting converts raw consumer variables into behavioral indicators. Based on this, such systems output legally compliant credit decisions. The entire process comprises 5 key components.

Data Ingestion and Normalization

This foundation layer aggregates and structures highly fragmented data streams from traditional credit bureaus and open banking APIs for alternative data credit scoring.

For instance, this stage includes combining completely divergent JSON structures from platforms like Experian and Plaid into a unified database schema.

In the case of skipping this step, the ML model trains on dirty data and corrupt variables. Missing values or field mismatches lead to inaccurate automated credit scores.

Feature Engineering

This process transforms raw data fields into predictive metrics that track borrower behavior over time.

A concrete lending example is calculating the precise days between payroll deposits to measure income regularity instead of looking at a flat bank account balance.

Without this step, the engine lacks deep context and relies purely on flat data points. And the system misses hidden indicators of deteriorating borrower behavior, such as debt cycling, due to these limitations.

Model Selection

This core layer of an AI loan decisioning system selects and executes the specific machine learning framework optimized to compute default probabilities across portfolios.

In production, this means using gradient boosting frameworks like XGBoost or LightGBM as the engine for high-concurrency lending decisions. When engineers skip rigorous model selection, they frequently rely on uninterpretable deep learning neural networks. They drive up compute costs and processing latency without any measurable lift in model accuracy.

Explainability Layer

This compliance gate translates abstract mathematical weights into human-readable, auditable drivers for every automated decision. For example, the system runs SHAP (Shapley Additive exPlanations) values to isolate and prove the top three data indicators that led to an individual loan rejection.

Without this layer, the credit engine operates as a legal black box. This makes it illegal to deploy in production under major global financial regulations.

Continuous Retraining and Monitoring

This maintenance pipeline constantly monitors model drift and schedules data updates based on real-world loan repayment cohorts.

The automated loan decisioning engine should undergo quarterly programmatic model adjustments. This process helps maintain alignment with changing macroeconomic indicators and purchasing trends.

Eliminating this pipeline causes the risk software to suffer from data drift, where a model trained on outdated historical conditions miscalculates risk on current applicant profiles.

How Does Tensorway Build an Automated Underwriting System?

At Tensorway, we have more than 7 years of experience in creating AI and ML-powered solutions, including machine learning credit scoring tools and AI agents for finance. Over this time, we’ve developed a smooth process that allows us to build custom products on time and on budget.

We structure our credit risk modeling machine learning development around specific milestone deliverables and focus on what your team receives at each phase.

- Data audit and strategy (weeks 1-2). You receive a structured data sourcing plan that covers your current data assets, verifies legal usability parameters, and isolates predictive signals for your specific borrower audience. This document flags critical data gaps and integration vulnerabilities.

- Feature engineering (weeks 2-4). We provide you with a verified repository of ranked predictive features tested directly against your historical loan repayment outcomes.

- Model development and benchmarking (weeks 4-8). Our experts prepare comparative validation reports that evaluate multiple candidate model architectures. We benchmark these engines against Area Under the ROC Curve (AUC), Gini coefficients, and algorithmic fairness metrics. This approach lets you review clear performance tradeoffs.

- Explainability and compliance layer (parallel track). You get an active SHAP integration blueprint and programmatic adverse action reason code templates. Apart from this, we also provide all technical documentation required under frameworks like the EU AI Act.

- Deployment and monitoring (final phase). At the end of the development process, our team delivers a production-ready scoring API endpoint, automated data drift alerts, and automated model retraining pipelines. This deployment architecture also includes a live performance dashboard. It can be directly used by risk managers without data science intervention.

What Will You Get with Your Custom AI Underwriting Software?

The complete implementation transfers full intellectual property ownership and operational control of the following core assets to you:

- Trained model artifacts (fully optimized weights tuned for your specific consumer loan product);

- scoring API (a low-latency microservice ready for direct integration into your existing loan origination system);

- feature importance documentation (complete mathematical blueprints detailing exactly how variables influence decisions);

- automated retraining scripts (programmatic execution pipelines to handle future credit cohort update cycles);

- explainability reports and compliance pack (audit-ready logs that contain deterministic SHAP outputs for regulatory verification).

Wrapping Up

A human review queue introduces a permanent trade-off between decisioning speed and strict risk compliance. With growing volumes of loan applications and increasingly stringent regulations, AI automation in financial services is becoming the most efficient way to address operational issues. Transition to automated loan decisioning eliminates structural bottlenecks and stops the applicant drop-off caused by manual processing delays.

Meanwhile, deployment of a compliant AI underwriting solution requires a well-structured process that includes multiple stages. If a development team skips a single step, from data normalization to introducing explainability gates, the entire system risks failing. Your production outcomes depend entirely on your machine learning tech partner.

At Tensorway, we have solid expertise in delivering AI agents and ML-powered systems for businesses in fintech, insurtech, and other dynamic domains. We are always open to cooperation and ready to discuss your project. Contact us, and we will help you find the right solution to optimize your underwriting workflows.

%20(1).jpg)